R Project - Implementing Black Scholes & Vasiciek Models

Implementing Black Scholes & Vasiciek Models to model the prices of European call options and bonds respectively.

Quick Summary

In this project we investigate the properties of financial stochastic processes. We first consider the implementation of the Black-Scholes model for determining the price of European call options on stock before then utilising the Vasicek model to calculate the future price of bonds. We discuss the background, benefits and drawbacks of both models before conducting our investigation and summarising our findings.

1 Introduction

The Black-Scholes model is a mathematical model developed by the economists Fischer Black, Myron Scholes and Robert Merton which is widely used in the pricing of options contacts. The model assumes that the price of heavily traded assets follows a geometric Brownian motion with constant drift and volatility. When applied to a stock option, the model incorporates the constant price variation of the stock, the time value of money, the option’s strike price, and the time to the option’s expiry.

The Vasicek model is a mathematical model used in financial economics to estimate potential pathways for future interest rate changes. The model states that the movement of interest rates is affected only by random (stochastic) market movements and models interest rate movements as a factor composed of market risk, time, and equilibrium value - where the rate tends to revert towards the mean of those factors over time.

We will first investigate how the price of a European call option - as given by the Black- Scholes model - varies with changes in time, interest rates, strike price and volatility. We will then simulate an Ornstein-Uhlenbeck process and use this to simulate the price of a bond - using the Vasicek model - over a given time period before evaluating the distribution of the simulated prices.

We conduct this project using the programming language R along with the ggplot2, reshape, tidyr and gridExtra packages.

|

|

2 The Black-Scholes Model

The price at time $t_0=0$ of a European call option (‘ECO’) on a stock with strike price $c$, expiry time $t_0$, initial stock price $S_0$, interest rate $\rho$ and volatility $\sigma$ is given by the Black-Scholes (‘BS’) formula, first derived in the article Black[1973]. This is given below in Equation 1:

\[\begin{aligned}P_{t_0}=&S_0\Phi\left(\frac{\log(S_0/c)+(\rho+\sigma^2/2)t_0}{\sigma\sqrt{t_0}}\right)\\ &-c\exp(-\rho t_0)\Phi\left(\frac{\log(S_0/c)+(\rho-\sigma^2/2)t_0}{\sigma\sqrt{t_0}}\right)\tag{1}\end{aligned}\]

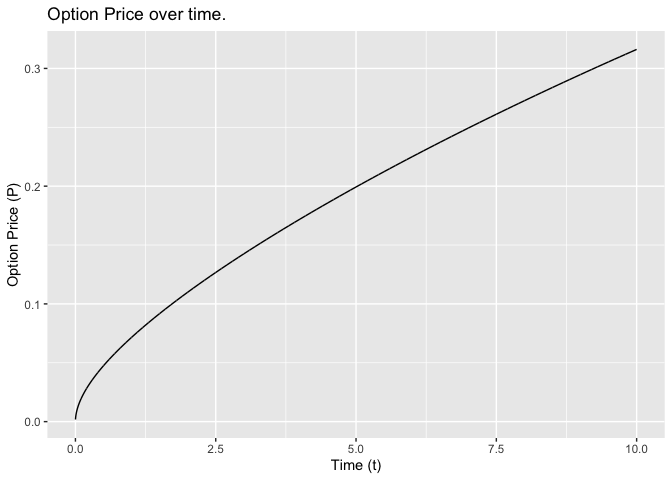

We plot the price over time of the ECO, $P_t$, for $0\leq t\leq 10$ with $s_0=1$, $\sigma^2=0.02$, $\rho=0.03$ and $c=1$. This is shown below in Figure 1.

|

|

We see that the price $P_t$ is increasing over time, which makes sense as the values of the ECO should be dependent on the time the underlying stock has to increase in value. From Equation 1 we can see that $S_0$ as $t\rightarrow\infty$.

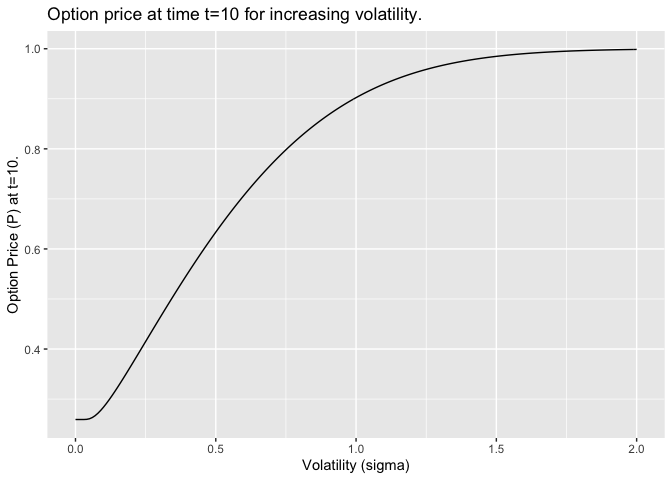

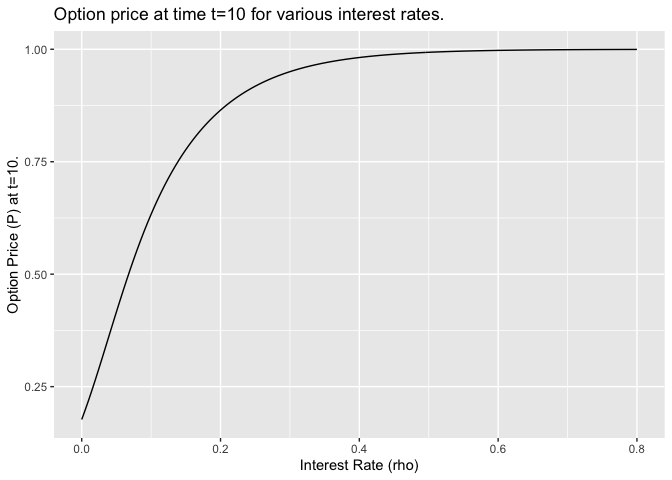

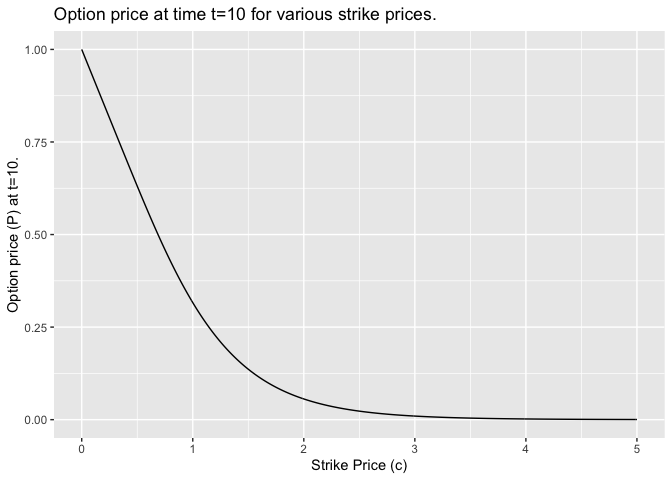

We plot the price $P_{10}$ at time $t=10$ as we vary each of $\sigma$, $\rho$ and $c$ in turn. These are shown below in Figures 2, 3 and 4 respectively.

|

|

As both volatility $\sigma$ and interest rates $\rho$ increase we see that $P_{10}\rightarrow S_0$. This is because high underlying stock volatility and interest rates both increase the potential option return which increases the options value up to the initial price of the stock. The option value is limited to this value because if the option price were to rise above the stock price then there would be no reason for investors to purchase the option rather than the stock.

As the strike price $c$ increases we see that $P_{10}\rightarrow 0$. This is because if the option has a high strike price it is less likely that the underlying stock will reach this price during the period of the option which makes the option less valuable.

3 Ornstein-Uhlenbeck Processes

The spot-rate ${R_s:s>0}$ is an Ornstein-Uhlenbeck (OU) process - with initial spot rate $R_0$, long-term mean $\mu$ and reversion speed $\theta>0$. This is given by Equation 2 below.

\[ R_s=e^{-\theta s}R_0+(1-e^{-\theta s})\mu+ X_s;. \tag{2} \]

Here, $X_s$ is an OU process with volatility $\sigma>0$ and reversion parameter $\theta>0$. This is equivalent to stating the following.

\[\begin{aligned} E[X_s]&=0 \\ Cov(X_s, X_t)&=\frac{\sigma^2}{2\theta}e^{-\theta(s+t)}e^{2\theta\min(s, t)-1} \end{aligned} \]

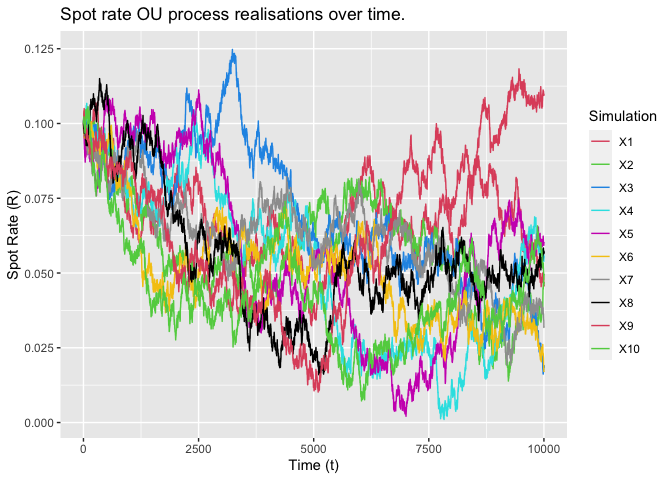

We simulate the OU process ${R_s:0\leq s\leq 10}$ for $R_0=0.1$, $\theta=0.5$, $\mu=0.05$ and $\sigma=0.02$ and produce a plot of our results. These are shown below in Figure 5.

|

|

The expressions for the mean and variance of this process are given by:

\[\begin{aligned}E[R_s]&=e^{-\theta s}R_0+(1+e^{-\theta s})\mu,\\V[R_s]&=\frac{\sigma^2}{2\theta}(1-e^{-s\theta s})\end{aligned}\]

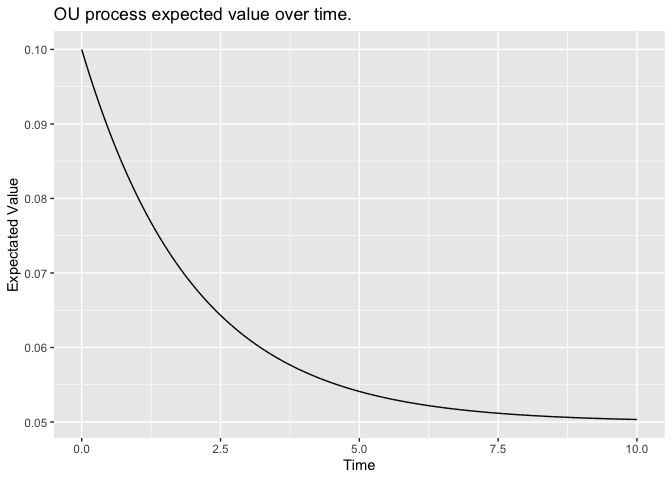

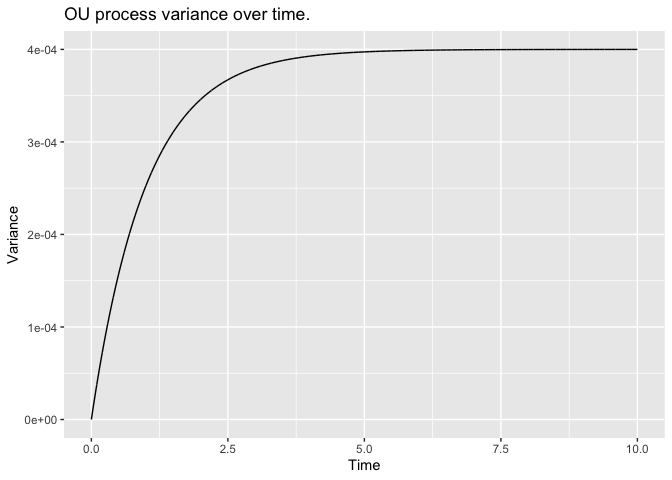

We plot the mean $E[R_s]$ and variance $V[R_s]$ against time in Figures 6 and 7 below.

|

|

From Figures 6 and 7 we evaluate what the mean and variance tend to as $s\rightarrow\infty$, for which we obtain the following expressions:

\[\begin{aligned}\lim_{(s\rightarrow\infty)}{E[R_s]}&=\mu\\\lim_{(s\rightarrow\infty)}{V[R_s]}&=\frac{\sigma^2}{2\theta}.\end{aligned}\]

We can see from Figure 6 that the expectation is tending towards the long-term mean $\mu=0.05$ as expected. We can also see from Figure 7 that the variance is tending towards 0.04, which is as expected per our expression for the limit of $V[R_s]$ as $s\rightarrow\infty$.

If we change the value of $R_0$ we will change the starting point of the process. If we change the value of $\mu$ we change the value which the expectation of the process will tend towards. If we increase the value of the reversion parameter $\theta$ only, we will decrease the value that the variance of the process will tend towards. Similarly, if we increase the value of the volatility $\sigma$ only, we will increase the value that the variance of the process will tend towards.

4 The Vasicek Model

The Vasicek model (first defined in article Vasicek(1977) and expanded in Burgess(2014)) defines the price $Q_t$ at time 0 of a bond paying one unit at time $t$. as:

\[ Q_t=\exp\left(-\int_0^t R_sds\right) \]

where $R_s$ is the OU process defined in Section 3.

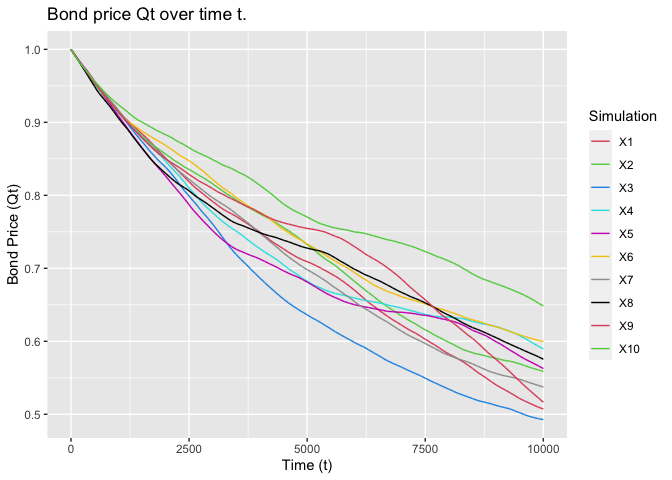

We plot 10 simulations of the bond price $Q_t$ at time 0 of a bond paying one unit at time $t$ for $R_0=0.1$, $\theta=0.5$, $\mu=0.05$ and $\sigma=0.02$. These are shown below in Figure 8.

|

|

We expect the distribution of $Q_t$ to be log-normal as the integral $\int_0^t R_s$ is normal - as it is a linear combination of normal random variables.

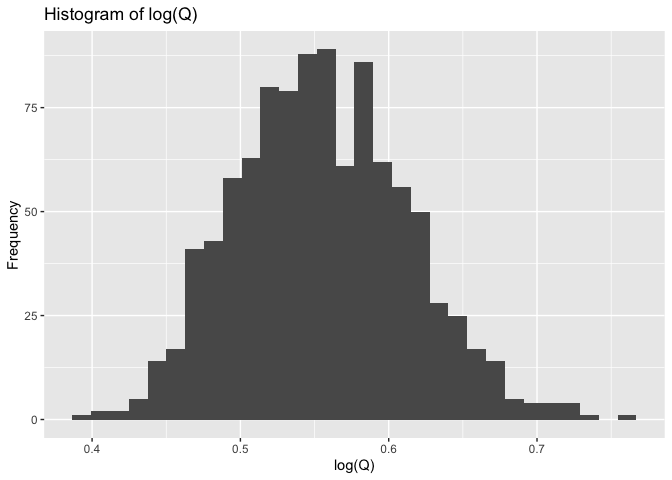

We can check the distribution of $Q_t$ for the fixed value of $t=0$ by simulating 1000 realisations of $\log(1_{10})$ and approximating their empirical distribution using a histogram - shown in Figure 9 below. From this histogram we can see that the distribution of $\log(Q_{t})$ appears to show the characteristic bell curve shape we would expect.

|

|

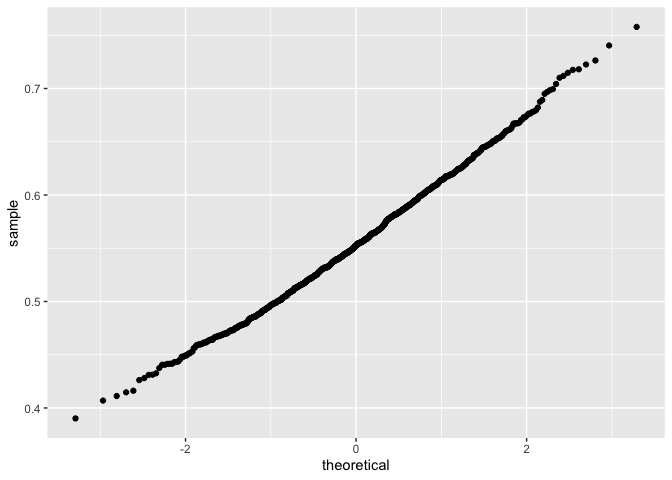

We can evidence this further by using a Q-Q plot to compare the empirical distribution we have simulated with the normal distribution - shown in Figure 10 below. From this plot we see clear evidence that the distribution is normal due to the linearity of the points generated.

|

|

5 Conclusion

Both models discussed in this project come with several limitations. Firstly, the Black- Scholes model assumes that an option can only be exercised at expiration which limits its use to European options (as US options can be exercised before expiration). The model also makes assumptions that do not tend to hold in real world applications such as that no dividends are paid out during the life of the option, that markets are efficient, that there are no transaction costs in buying the option, that the risk-free rate and volatility of the underlying assets are known and constant and that the returns on the underlying assets are known and constant. (Hull[2003])

The main disadvantage of the Vasicek model that has come to light since the global financial crisis is that the model does not allow for interest rates to dip below zero and become negative. This issue has been fixed in several models that have been developed since the Vasicek model such as the exponential Vasicek model and the Cox-Ingersoll-Ross model for estimating interest rate changes and further investigation into these models would be a useful topic of further research.